"It is estimated that China's share of the global market will exceed 60% in 2020, and the diaphragm will be fully localized and exported to the global market." This is the conclusion of a research report by Guosen Securities Economic Research Institute in a research report. According to the institute, the data shows that China's lithium battery separator production capacity will reach 10 billion square meters in 2020.

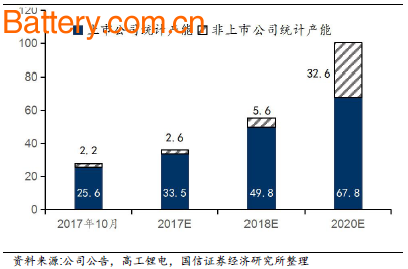

The data shows that in domestic companies (including A-shares and NEEQ) or companies controlled by listed companies, they currently have a capacity of 2.56 billion square meters (sum of dry and wet diaphragms). And with the capacity to start production by the end of 2017, Guosen Securities expects to reach 3.61 billion square meters of diaphragm capacity this year. The number of large-scale diaphragm companies in the non-listed system is small, and most of the planned investment capacity will not be released until after 2018. According to statistics from Guosen Securities, the total production capacity of lithium battery separators in China will reach 1.04 billion square meters by 2020, of which the statistical production capacity in the listed company system will reach 6.78 billion square meters, and the statistical capacity in the non-listed company system will reach 3.26 billion square meters.

Guoxin Securities believes that the diaphragm is an important part of the lithium batteries in recent years with the rapid decline in the price of domestic diaphragm successful in accounting for the total cost of lithium battery materials also declined, generally around 7-15%. Generally speaking, since the unit cost of the positive electrode and the negative electrode material in the ternary battery is relatively high, the cost of the separator accounts for less than 10%, and the unit cost of the positive and negative electrode materials in the lithium iron phosphate battery is relatively low, and the cost of the separator accounts for about 15%. Among the lithium battery materials, the barrier technology barrier and gross profit margin are relatively high, and it is also the last material to achieve localization.

Global market share will be concentrated in China

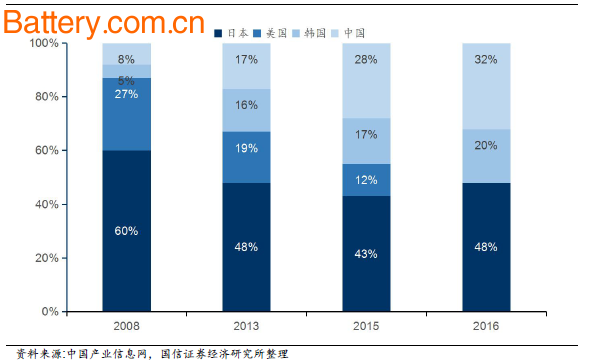

The global market share of lithium battery separators is mainly occupied by Japan, the United States, South Korea, and China. However, with the acquisition of Celgard by Japan in 2015, the United States has withdrawn from the lithium battery market (Celgard market share is still included in US companies in 2015). With the breakthrough in the preparation process of lithium batteries in the research institutes represented by Sichuan University in recent years, coupled with the large capital investment of production companies, China’s global lithium battery separator market share has increased rapidly. In 2016, global diaphragm shipments were Around 3.38 billion, China's shipments reached 1.084 billion, and the global market has reached 32%. In the future, with the production of a large number of wet diaphragm production capacity, Guosen Securities expects that China's global market share will exceed 60% in 2020, achieving a comprehensive localization of the diaphragm and exporting to the global market.

Global lithium battery separator shipments accounted for changes (unit: %)

At present, Japan's diaphragm manufacturers mainly include Asahi Kasei (acquisition of Celgard), Dongyan (with diaphragm manufacturing plant with Toray), Ube and Sumitomo Chemical. The diaphragm manufacturers in Korea are mainly SK innovation and W-scope. In recent years, with the rapid growth of the global lithium battery market, foreign lithium battery separator manufacturers have also expanded their production capacity. For example, Asahi Kasei announced an investment of 15 billion yen in March 2017, and plans to build 200 million square meters of wet diaphragm capacity in 2019. Sumitomo Chemical of Japan plans to expand its current production capacity by four times. In 2018, its production capacity will reach 400 million square meters. South Korea's W-scope announced in September 2016 that it will invest 30 million US dollars to build a new production line in South Korea. It is expected to reach 300 million square meters by the end of 2018.

The Chinese market is growing rapidly and the industry landscape is changing rapidly.

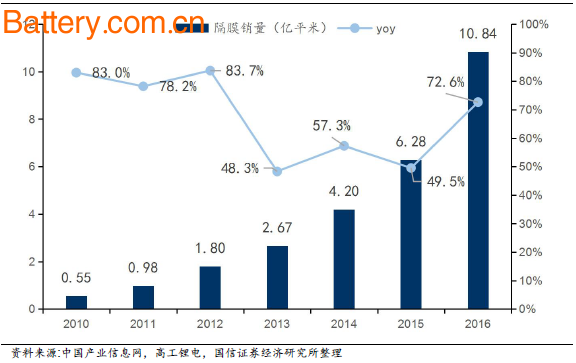

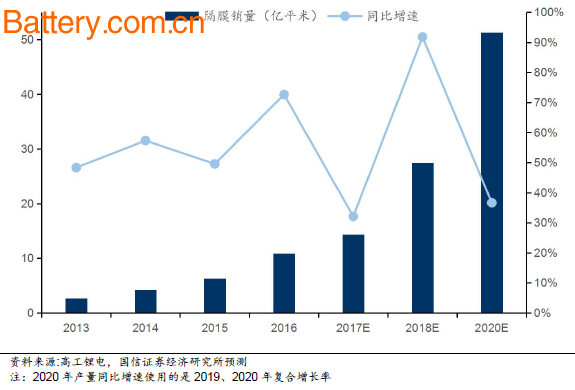

China's development of lithium battery separator technology is later than foreign companies. From the successful commissioning of the first production line of Xinxiang Gryen Company in 2004 and the production of qualified products, Chinese enterprises have developed rapidly in the lithium battery separator industry in the past decade. Especially after 2010, driven by the new energy automobile industry chain, the lithium battery industry developed rapidly. China's diaphragm sales increased rapidly from 0.55 billion square meters in 2010 to 1.084 billion square meters in 2016, with a compound annual growth rate of 64.3%.

Annual sales volume and year-on-year growth rate of lithium battery separators in China (unit: 100 million square meters, %)

Compared with foreign companies, the diaphragms produced by domestic enterprises are mainly dry stretching, and most of them are medium and low-end products. High-end wet diaphragm has been monopolized by foreign companies for many years. However, in recent years, with the continuous improvement of the domestic diaphragm production enterprises in the wet production process, the output and performance of the wet diaphragm are getting closer to the level of foreign enterprises. Domestic enterprises have rapidly expanded the wet diaphragm, and the diaphragm market has also occurred. Variety.

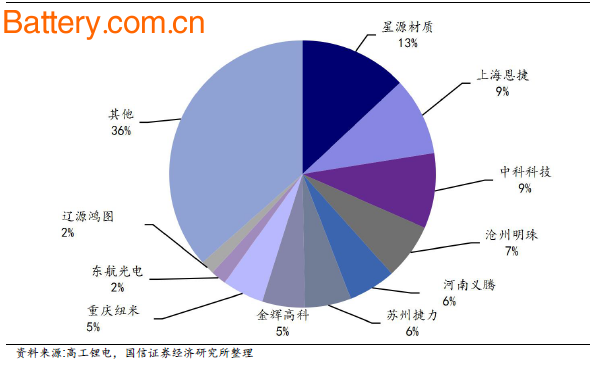

In 2012, domestic enterprises mainly produced dry-process membranes. Xinxiang Grein, Xingyuan Materials, Foshan Jinhui, Shandong Zhenghua, and Foshan Shandong Airlines occupied the top five in the domestic market, while in 2016, domestic production of wet-membrane-based Shanghai Enjie, Suzhou Jieli, Jinhui Hi-Tech, Chongqing Newmi and other companies ranked first in the shipments.

In 2016, the market share of the top ten enterprises in China's lithium battery separator shipments reached 63.50%. It is expected that the market concentration will further increase with the gradual production of production capacity of major enterprises in the future.

2016 China lithium battery separator market share (unit: %)

The foreign diaphragm market is mainly based on the expansion of existing enterprises. There are few new entrants, and the domestic diaphragm market is driven by capital. Not only a large number of enterprises have expanded their production, but also new entrants are still being promoted by big funds. In the diaphragm market, data show that China's lithium battery separator production capacity will reach 10 billion square meters in 2020.

Market space: new energy vehicles drive the rapid growth of diaphragm demand space

As an important strategic industry in China, the promotion and popularization of new energy vehicles is of great significance for improving China's energy consumption structure and reducing the dependence of foreign oil on foreign countries. In the previous series of reports, Guosen Securities has focused on the analysis of the “subsidy retreat + points system†policy, the new energy vehicle industry will gradually be guided by the government to market competition.

In the long run, the new energy auto industry is currently in the early stage of industrial development, and the industry has huge room for development. According to relevant national plans, China Automotive Technology and Research Center predicts that by 2020 and 2025, sales of new energy vehicles will reach 2 million and 7 million, respectively, accounting for 7% and 20% of total vehicle sales respectively.

Guosen Securities analyzed in detail the production forecast process for new energy passenger cars, buses and special vehicles during 2017-2020. Although the fraudulent incident at the end of 2016 cast a shadow over the development of the new energy automobile industry, the growth rate of new energy vehicles in the second half of the year continued to accelerate in the second half of the year under the driving force of the industrial trend and the expectation of the new double-point policy. It is estimated that the annual output will reach 660,000 units, and the annual production growth rate is 28.75%.

Based on the rapid growth of new energy vehicles, the demand for power batteries has also increased rapidly. Due to the rapid increase in sales of small-capacity models in the first half of the year, the number of bicycle battery-equipped vehicles in passenger cars has declined. However, Guosen Securities considered that some large-capacity new models will be launched in the second half of the year, and the decline trend of pure electric passenger car battery-equipped vehicles has slowed down, and is expected to decline by -6% for the whole year. After 2018, with the production of large-capacity battery models of mainstream automakers (the battery life is basically 300km), the number of bicycle battery packs will maintain steady growth in the future.

The high-energy new energy vehicle market will directly drive the demand for power batteries. According to detailed forecasts, Guosen Securities expects that the demand for power batteries in 2018-2020 will reach 52.89GWh, 74.97GWh and 120.85GWh, respectively, with a compound annual growth rate of 32%.

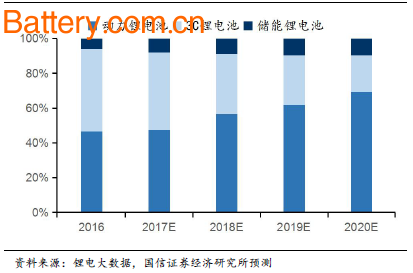

In addition to the power battery of new energy vehicles, lithium battery is mainly used in the field of 3C products and energy storage batteries. 3C electronic products as the traditional applications of lithium batteries, occupy the mainstream demand for lithium batteries, but with the growth of the mobile phone market slowed, laptop and tablet market approaches saturation, 3C electronic products accounted for lithium batteries In 2016, it was exceeded by power battery for the first time. Guosen Securities expects the growth rate of lithium batteries for 3C products to be between 5 and 7% between 2017 and 2020. By 2020, the total demand for lithium batteries for 3C products is expected to reach 36.6GWh.

Energy storage batteries are another important growth point in the lithium battery market. With the country's emphasis on new energy and energy storage industries, a number of policies and plans have been launched in recent years to vigorously promote the construction of energy storage systems. This has also accelerated the application of lithium batteries in the energy storage market. In the Chinese energy storage market in 2015, the installed capacity of lithium-ion batteries accounted for 66%, followed by lead batteries and flow batteries. According to the prediction of lithium battery data, the demand for lithium battery energy storage in China will reach 16.64GWh in 2020.

Combined with the demand forecast for three areas of power battery, lithium battery for 3C products and lithium storage battery, Guosen Securities expects that the total demand for lithium batteries will reach 174GWh by 2020, accounting for 69.4 in these three fields. %, 21.0%, 9.6%.

Demand forecast for lithium batteries for 2017-2020 (unit: GWh)

2017-2020 lithium battery structure ratio forecast (unit: %)

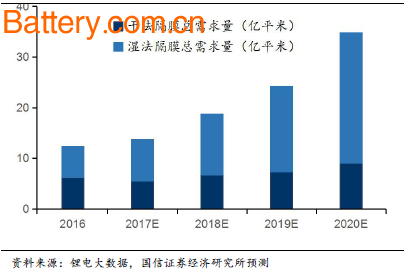

According to the actual production situation, about 0.25 million square meters of lithium battery separators are required for each GWh of electricity. Therefore, Guosen Securities expects that the total demand for diaphragms in the domestic lithium battery market will reach 3.48 billion square meters in 2020. Dry membranes and wet membranes have different permeability rates in different fields of demand. In the field of power batteries, as the country has increased the requirements for the mileage of new energy vehicles, under the guidance of policy guidance, major battery manufacturers tend to produce ternary batteries with higher energy density and thinner lithium battery separators. After considering the actual needs of various models, Guosen Securities expects that the proportion of ternary batteries in power batteries will reach 77.66% by 2020 (the detailed analysis process in the series report 1), while the ternary battery in the power battery is almost Wet diaphragms are used, so Guosen Securities expects the permeability of the wet diaphragm to be consistent with the permeability of the ternary battery. Due to the higher thickness requirements of the lithium battery for 3C products, Guosen Securities expects that the penetration rate of wet diaphragm in lithium batteries for 3C products will reach 90% by 2020. In the energy storage lithium battery, the current lithium iron phosphate battery is still the mainstream. Because the energy storage lithium battery does not require high energy density, Guosen Securities expects that the wet diaphragm permeability in the energy storage lithium battery will be about 20% by 2020. . Based on the above analysis, Guosen Securities expects that the domestic demand for wet diaphragm will reach 2.58 billion square meters by 2020, and the demand for dry diaphragm will reach 90 million square meters.

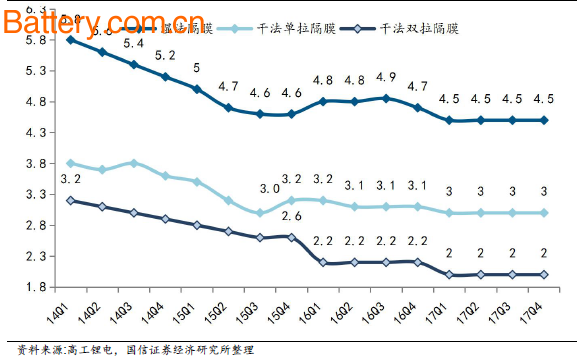

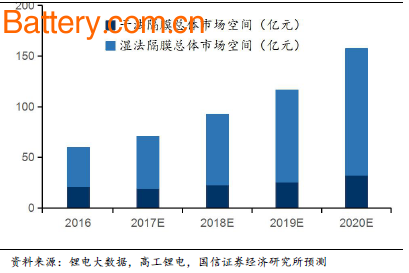

In 2016, the average market price of dry and wet diaphragms was 3.0 yuan / square meter and 4.8 yuan / square meter respectively. After coating, the price of the diaphragm can be increased by 2 yuan / square meter. Considering the rapid expansion of domestic diaphragm production capacity and the spatial proportion of dry and wet methods in the future, Guosen Securities conservatively predicts that by 2020, the average market price of dry and wet diaphragms will reach 2.6 yuan / square meter and 3.3 yuan / square meter respectively. The price after coating is 4.3 yuan / square meter and 4.8 yuan / square meter. In the end, Guosen Securities expects that China's diaphragm market will reach 15.75 billion yuan in 2020, of which the market space for dry and wet membranes is 3.25 billion yuan and 12.5 billion yuan respectively.

2017-2020 diaphragm demand forecast (unit: 100 million square meters)

2017-2020 diaphragm market space forecast (unit: 100 million yuan)

Industry trends: wet law into the mainstream, more intense competition

At present, the production processes on the market are mainly dry uniaxial stretching technology, dry biaxial stretching technology and wet stretching technology. Compared with the three methods, the dry uniaxially stretched diaphragm has poor lateral strength, but has high safety due to almost no heat shrinkage. The dry biaxial stretching process can only produce a single layer of separator, but the pore size and distribution of the separator are not uniform and the stability is poor. The wet stretched membrane has higher porosity and gas permeability, and can produce a thinner and thinner diaphragm, but the investment cost is higher.

Compared with the dry stretching film forming process, the lithium battery separator made by the wet process can be made very thin, and the program control method is not by mechanical stretching, but by the thermal phase of the polyethylene and the pore forming agent. The fear of separation, so the porosity and pore size are easier to control, the mechanical properties and uniformity of the product is better. It can be seen from the comparison of the microscopic morphology that the pore size in the film formed by dry stretching is distributed in a certain direction, and the crystalline and amorphous regions of the film are clearly separated, and the wet process is made. The topography of the diaphragm is significantly more uniform.

After the national new energy tram policy has increased the requirements for vehicle weight and cruising range, it is an important development direction to improve the unit charge of the power battery under the premise of ensuring safety. Guoxin Securities listed the influence of various performances on battery performance in Table 1 above. In general, the advantages of wet process with thinner thickness, better uniformity and easier control of pore size are more obvious.

The raw material for the dry process is generally PP, while the raw material for the wet process is generally PE. Generally, the melting temperature of PP is about 170 ° C, and the melting temperature of PE is about 140 ° C. Therefore, although the separator produced by the wet process is thin, the lower melting temperature makes the separator easily shrink at a high temperature, thereby causing a short circuit of the battery, and the safety of the battery is not guaranteed. Coating a layer of inorganic nanoparticles or high temperature resistant organic chemicals on the surface of the separator can improve the high temperature safety performance of the separator and can make up for this defect in the wet process.

Depending on the product requirements, the diaphragm can be coated on one side or on both sides, usually at a thickness of 1-2 um. The coated separator not only improves the heat shrinkage rate, but also increases the tensile strength and the liquid absorption rate while reducing the porosity and the gas permeability. The higher tensile strength of the separator can improve the controllability of the cell, and the lower heat shrinkage can make the battery safer at higher temperatures. The relatively small porosity can reduce the short circuit rate of the cell, and the liquid absorption rate can help. To increase the energy density of the battery. Diaphragm manufacturers typically use different coating materials based on downstream requirements, and the base film + coating technology provides customizable capabilities for diaphragm products.

Because the wet diaphragm is thinner, and its high void ratio and air permeability can make the battery have higher energy density and charge and discharge performance, after the coating improves the safety performance, it makes up for the short plate of the wet diaphragm and begins to become more and more. Many are used in the power battery of new energy vehicles. In the future, under the development trend of electric vehicles to improve the cruising range, with the improvement of the localization rate of wet diaphragm and the reduction of the production cost of wet diaphragm, Guosen Securities expects more and more power lithium batteries will use wet diaphragm + Process solution for multi-functional material coating.

Future wet capacity expansion will be much larger than dry method

Guosen Securities has compiled all the information on the public information that can be found in the production of lithium battery separators by 2020. The data shows that in domestic companies (including A-shares and New Third Board) or companies controlled by listed companies, With a capacity of 2.56 billion square meters (sum of dry and wet diaphragms). And with the capacity to start production by the end of 2017, Guosen Securities expects to reach 3.61 billion square meters of diaphragm capacity this year. The number of large-scale diaphragm companies in the non-listed system is small, and most of the planned investment capacity will not be released until after 2018. According to statistics from Guosen Securities, the total production capacity of lithium battery separators in China will reach 1.04 billion square meters by 2020, of which the statistical production capacity in the listed company system will reach 6.78 billion square meters, and the statistical capacity in the non-listed company system will reach 3.26 billion square meters.

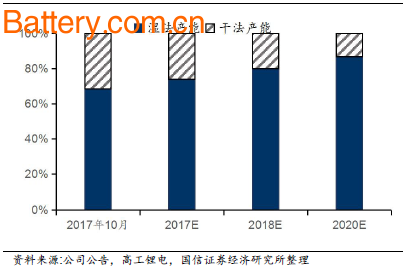

It is worth noting that, in the new capacity that will be put into production before 2020, according to the statistics of Guosen Securities, the dry capacity is only 470 million square meters of new capacity (of which only 230 million is clearly put into operation in the listed company system). In the same period, the newly added wet diaphragm production capacity will be 6.79 billion square meters.

Therefore, with the large-scale production of wet process capacity in the future, Guosen Securities expects that the proportion of wet process capacity in domestic diaphragm production capacity will increase from the current 69% to 87% in 2020. Although the dry diaphragm is shipped slightly more than the wet diaphragm in 2016, with the gradual release of the wet diaphragm capacity from 2017, the wet diaphragm will occupy an increasing proportion in the future diaphragm market.

2017-2020 industry-wide diaphragm statistical capacity (unit: 100 million square meters)

2017-2020 dry and wet diaphragm production capacity (%)

According to the average output rate of the good diaphragm production line (sellable diaphragm products) in the industry is about 60%, Guosen Securities forecasts the production of diaphragms in the next few years. In this forecast, Guosen Securities has made the following premise:

1. The production line that has been put into production at present, taking into account the different production time, the overall expected annual output rate is 50%;

2. The production line newly put into production before the end of 2017 is expected to have a production rate of 5% this year;

3. In the production line newly put into production in 2018, the average output rate is expected to be 30%, taking into account the overall production time.

4. The production line newly put into production in 2019-2020, considering the uncertainty of the production time, is expected to have an average output rate of 40% in 2020.

After calculation, Guosen Securities expects the diaphragm production in 2017 to be 1.43 billion square meters. In the future, when the new capacity is put into production smoothly, the diaphragm production of domestic enterprises is expected to reach 2.75 billion square meters in 2018, and it is expected to reach 5.12 billion square meters in 2020.

Domestic wet diaphragm production and growth forecast for 2017-2020 (unit: 100 million square meters, %)

Under the full competition, the price of the diaphragm is lower.

According to Guoxin Securities' calculation of total domestic diaphragm production and total demand, domestic diaphragm production in 2017 is generally close to demand, considering that the demand for wet diaphragms in the market is significantly higher than that of dry diaphragms. Guoxin Securities believes that the supply and demand pattern of wet diaphragms in the market in 2017 is still tight. From 2018 onwards, according to the calculation of Guosen Securities, the total output of the domestic diaphragm will exceed the demand in the case of smooth production of various enterprises.

Domestic diaphragm production and total demand forecast for 2017-2020 (unit: 100 million square meters)

With the increase in diaphragm supply in the market, Guosen Securities believes that competition in the diaphragm market will intensify in the future. In particular, the rapid expansion of wet process capacity will put a lot of pressure on the prices of wet and dry diaphragm products. On the one hand, diaphragm companies will compete with each other. On the other hand, wet diaphragms will also occupy the dry diaphragm. Market space. After 2018, the price of diaphragm products will gradually decline, which is an inevitable trend. The decline in price is mainly determined by the progress of production capacity.

China lithium battery separator average price change (Unit: yuan / square meter)

Along with the lower price of diaphragm products and the rapid expansion of domestic diaphragm production capacity, Guosen Securities believes that the domestic diaphragm will have a strong impact on the global market, and the low-end diaphragm market will be fully localized and even exported. In 2016, the domestic lithium battery production value accounted for about 50% of the world, and the foreign market still has a large export space to accommodate some of the newly built domestic production capacity.

Investment points: The industry's growth period focuses on the progress of production

In the field research interviews with diaphragm manufacturers, Guosen Securities also learned that in the future development of the industry, expanding production scale, optimizing equipment technology, and reducing production costs will be the focus of business operations, especially to rapidly expand production scale and seize customer resources. It is the most important thing. Because the larger the scale of production, it can meet the procurement needs of large battery companies. The larger the order quantity of the same performance diaphragm purchase quantity, the fewer the parameter adjustment times of the preparation equipment can be reduced, the loss of the production process can be reduced, and the equipment operation can be improved. Efficiency, reducing the unit depreciation cost of the equipment. For stable production enterprises, the diaphragm costs mainly include raw materials (PP/PE, paraffin oil, methylene chloride, etc., accounting for 30-40%), labor (about 10-20%), and energy (about 10%). -20%), equipment depreciation (20-30%).

PP and PE in the raw materials are the basic raw materials for the separator, which is generally related to the yield of the separator. The higher the yield, the smaller the loss and the lower the unit cost. UHMWPE used in wet diaphragms is generally purchased from abroad, and price fluctuations are more consistent with fluctuations in crude oil prices. The unit cost of paraffin oil and methylene chloride fluctuates greatly, because paraffin oil and methylene chloride can be recycled and reused after high temperature distillation, scraper vacuum evaporation, and the company can improve the recovery efficiency and reduce the unit cost through process optimization. . The unit cost of depreciation of various enterprise equipment also varies greatly, because the mainstream production equipment of domestic diaphragms is often imported from Japan, South Korea, Germany, Italy and other countries. In addition to the cost of procurement, the production efficiency of each production line and the processes of various enterprises Optimization is different.

Guosen Securities has made a statistical analysis of the distribution relationship between gross profit margin, net interest rate and operating income of some diaphragm manufacturers in recent years. After eliminating the annual data of losses and the annualization of the 2017 data, we can see that the profitability of the diaphragm industry has a close relationship with the scale of operating income. When the operating income is small, the gross profit margin and net profit margin of the enterprise are mostly distributed. It generally means that the production line is small or the new capacity is not completely released. When the operating income exceeds 200 million yuan, the enterprise's gross can be observed. Both interest rates and net interest rates can be maintained at a relatively stable level, which means that after reaching the above scale, the unit production cost of the diaphragm and the intermediate rate of the enterprise will be significantly reduced. According to the current average price of dry and wet diaphragms, only when the diaphragm sales volume exceeds 50 million square meters, it means that the company's production and operation can achieve a relatively stable profit.

The process technology of wet diaphragm has higher threshold

In the future, the investment capacity of wet diaphragm is much higher than that of dry diaphragm. Therefore, Guosen Securities mainly analyzes the influence of the technology of wet diaphragm on the production efficiency and product cost of the enterprise.

Although the preparation process of the lithium battery separator is similar to the process of the conventional packaging film such as BOPP, BOPA, the difference is still large, and the new entrant is difficult to master the core process in a short time.

The process steps of the dry process are long, and the key point is the stretching of the separator into a pore after heat treatment. Although the wet process has fewer production steps, the ingredients, extrusion film formation, extraction, heat setting and other aspects will affect the performance quality of the product. China's diaphragm industry began to break through from the dry process of film making, high-end wet diaphragm has long been monopolized by Japanese companies such as Asahi Kasei and Toho. Until the breakthrough in the preparation process of scientific research institutes represented by Sichuan University Laboratory in recent years, all enterprises have entered the field of wet diaphragm production. Many enterprises have also optimized the process according to actual production conditions. Great progress.

The impact of the diaphragm production process on the unit cost of the product mainly reflects the optimization of each production link. For example, after the separator is wound into a parent roll, it will be classified into product A (for customer sales), product B (price reduction), and waste (disposal) according to performance requirements. It will also be cut according to the customer's needs. Some of the separators need to be cut twice after the coating process. The optimized and reasonable enterprises can achieve a comprehensive yield rate of 80%, and the enterprise yield rate is not up to the mature technology. 50%. The difference in yield rate directly affects the unit cost of raw materials for the product, as well as the depreciation and amortization unit cost of the fixed assets.

The optimization of the production process, in addition to improving the yield rate, can also increase production efficiency by increasing the output per unit time of production equipment, and reduce the unit cost of depreciation and amortization of fixed assets. Taking the equipment imported from Japan as an example, the design speed of the equipment is generally 35 m / s, the annual production capacity of single line is about 60 million square meters, and some manufacturers can set the production speed to 55 after optimization of process and equipment. In meters per second, the annual production capacity of a single line can reach 90 million square meters.

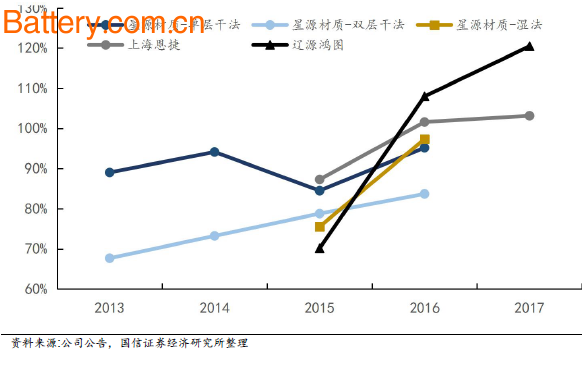

Therefore, the degree of mastery of each company's production process will directly affect the unit cost of diaphragm products. Guosen Securities selected data on the utilization rate of membrane capacity of some enterprises in recent years. It can be seen that the capacity utilization rate of the wet process of Shanghai Enjie, Liaoyuan Hongtu and Xingyuan materials, which are mainly based on the production of wet diaphragms, is obvious with the prolonged production time. Improvement. This shows that the process technology threshold of the wet diaphragm diaphragm is still high. Only after a period of process integration and optimization and improvement can the enterprise gradually increase the capacity utilization rate, and even achieve the capacity utilization rate exceeding 120%.

Changes in membrane utilization rate of some enterprises (unit: %)

Investment efficiency affects profitability

At present, domestic wet diaphragm production equipment is mainly imported from abroad. The production cycle, investment cost and output efficiency of different equipments are quite different, which also has a great impact on the operation status of diaphragm manufacturers. Major foreign equipment suppliers are mainly Japanese steel mills and Toshiba, South Korea's Master and MyungSung, Germany's Bruckner and France's Esop. Domestic equipment manufacturers generally supply auxiliary equipment, with Dalian rubber and plastics. Enterprises such as Guilin Automation Institute and Zhongke Hualian can provide some equipment or assist in equipment transformation.

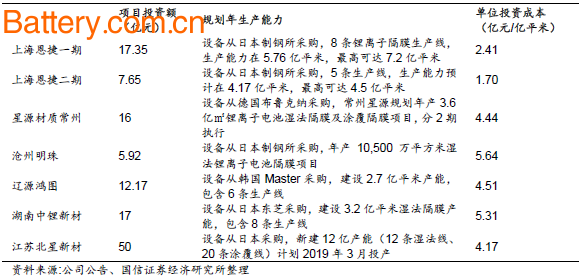

Compared with the investment efficiency of new capacity of some enterprises, the investment cost of Shanghai Enjie is significantly lower than that of other companies, mainly because the company optimizes the process and the output efficiency of single line is higher. The unit investment cost of other companies is basically at the level of 4.5-550 million yuan / 100 square meters, according to the annual depreciation rate of the average production equipment of each enterprise of about 8%, the unit depreciation cost of the diaphragm can reach 0.44 yuan / square meter, which Cost pressure is still high for companies. Therefore, only by increasing the production efficiency of the equipment or reducing the annual depreciation rate of the equipment in financial auditing can the proportion of equipment depreciation in the production cost of the diaphragm be reduced.

Comparison of investment efficiency of some company planning projects

Comparison of depreciation of mechanical equipment in some enterprises

China Strong Adhesive,Super Glue Gel manufacturer, choose the high quality Super Glue For Plastic,Glue Gel, etc.

Strong Adhesive,Super Glue Gel,Super Glue For Plastic,Glue Gel

KRONYO United Co., Ltd. , https://www.taibeikronyo.com